Indian Economy has exhibited robust growth over the past few decades thanks to a

strong well regulated financial sector. This was demonstrated when Indian Economy

withstood the ripple effects of global financial meltdown of late 2007. The culprit of

the global financial meltdown can be traced to instruments called Collateralized Debt

Obligation and various complex derivative products meant to disperse risk traded in

a poorly regulated financial market. We have to understand that the poor regulatory

environment is biggest culprit. Indian economy has also faced its share of repercussions

of the meltdown.

India has been in the path of rapid development since late 1960s following

nationalization of 14 major banks. Banks grew in size and extent, credit growing at an

average annual rate of 19% till 1980s. In order to address the concerns over asset

quality and to adopt international norms “The Committee on Financial System” more

popularly known as Narasimham Committee was setup.

Out of various recommendation of the Committee one of them dealt with creation of an

Asset Creation Fund to which public sector banks would transfer their Non-performing

assets with certain safeguards. This was the first instance of allowing securitization

in India. However the recommendation was not accepted and banks were required to

manage NPA internally.

The idea of securitization first envisaged in the United States, in 1980s, when finance

majors like Freddie Mac and Fannie Mae issued securities to investors which were

backed by mortgage loans. At that time banks were finding it increasingly difficult to

finance the growing demand for home loans from deposits and debt that they liquidated

their loan assets by transferring it to a Special Purpose Vehicle (sponsored by the

financial institution)

Legal system adopted in India

Meanwhile, in India, during 1980s asset quality started becoming a cause of concern.

The Government had resorted to various mechanisms for managing NPA like

Sick Industrial Companies (Special Provisions) Act 1985: under which Board for

Industrial and Financial Reconstruction (BIFR) was set up. However the whole process

was cumbersome and inefficient.

Recoveries of Debt due to Bank and Financial Institutions Act, 1993: under which

Debt Recovery Tribunal was set up. However the recovery process was slow and

the stringent requirement of the act rendered attachment and foreclosure of assets

ineffective.

Corporate Debt Restructuring System: A transparent system for restructuring loan

payments to meet project cash flow was provided for. This was effective, but it only

provided for deferring the cash flow, thus the loan remained in the balance sheet.

Securitization and Reconstruction of Financial Asset and Enforcement of Security

Interest Act, 2002: under which formation of Securitization Companies and Asset

Reconstruction companies have been legalized and secured creditor is empowered to

enforce security interest without intervention of court

SECURITIZATION ; An Introduction

Simply put, under this process, assets with predictable stream of cash flows are pooled

together to distribute risk and repacked into securities with predetermined returns.

In order to understand Securitization process clearly, it is imperative to know various

parties to the Securitization process. The parties involved are

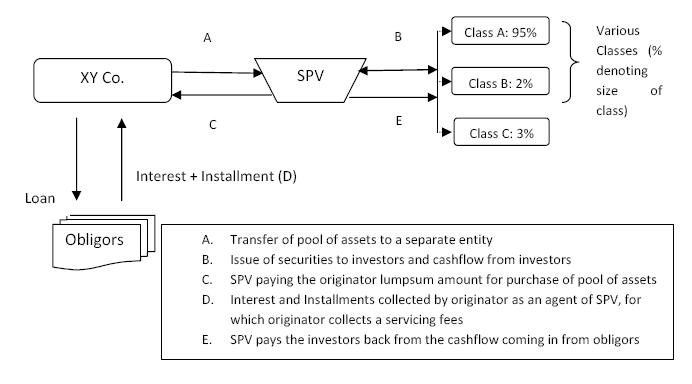

(i) Originator: The entity in whose books the assets to be securitized exist

(ii) Special Purpose Vehicle (SPV): This entity buys the assets to be securitized from

the Originator and makes payment to the Originator. This may be sponsored by a

financial institution interested in securitization and reconstruction business.

(iii) Investors: Persons like Financial Institutions, Mutual Funds, Pension Funds,

Insurance Company etc… investing in the securities issued by SPV. They

receive periodic return as per the agreement

(iv) Obligor or Borrower: This is the originator’s debtor from whom the loan amount is

due.

(v) Trustee: Those who oversee the activities of the trust to look after the interests of

the investors.

Additionally there may also be a rating agency engaged to assess the credit risk of the

security, an administrator or servicer to collect the payment due from the Obligor and

pass it to the SPV and a structurer to bring together the Originator, Investors and other

parties to a securitization deal.

SECURITIZATION; the ProcessUnder this process, also called structured finance, certain securities with predetermined

return are issued by a Special Purpose Vehicle formed for the purpose. The return

and final repayment of principal depends on cash flow generating capability of the

underlying pool of assets. The SPV can be a trust, company or partnership firm. The

SPV purchases the assets from the originator (bank or financial institution). The SPV

thus becomes entitled to the cash flow generated by the assets. This cash flow will be

repackaged to issue the security in the form of bond/debenture with predetermined

return.

Any asset that generates predictable stream of cash flow can be securitized like Credit

card receivables, Vehicle Loan receivables, equipment loan receivables, home loan

receivable, education loan receivables and even premium receivable for risk undertaken.

The Securitization process employs risk management methods similar to an insurance

company. At least some of the assets purchased may have a risk of becoming non-

performing; however pooling a large number of different types of loan assets significantly

reduces the overall risk. Loan portfolios of different quality and return are mixed in

varying proportions by the securitization company to create bonds/debenture falling

under different risk levels.

Individual securities are often split into tranches, or categorized into varying degrees

of subordination. Each tranche has a different level of credit protection or risk exposure

than another: there is generally a senior (“A”) class of securities and one or more

junior subordinated (“B,” “C,” etc.) classes that function as protective layers for the “A”

class. The senior classes have first claim on the cash that the SPV receives, and the

more junior classes only start receiving repayment after the more senior classes have

repaid. Because of the cascading effect between classes, this arrangement is often

referred to as a cash flow waterfall. In the event that the underlying asset pool becomes

insufficient to make payments on the securities (e.g. when loans default within a portfolio

of loan claims), the loss is absorbed first by the subordinated tranches, and the upper-

level tranches remain unaffected until the losses exceed the entire amount of the

subordinated tranches. The senior securities are typically AAA rated, signifying a lower

risk, while the lower-credit quality subordinated classes receive a lower credit rating,

signifying a higher risk. The return offered by the security will also depend on maturity,

cash flow pattern, prepayment and interest duration of underlying loan assets.

Advantages of SecuritizationSecuritization accelerates the cash inflow from loan thus not only providing immediate

liquidity but also ease the strain on capital adequacy. Assets Reconstruction Companies

also enable banks to focus on areas of core competency by shifting monitoring and

management of NPAs to them

Securitization offers the flexibility in structuring and timing cash flows to each security

tranche. It provides means whereby customized securities can be created to match the

tenure of assets and liabilities. Securitization also helps the originator to diversify its

funding source, by selling it to global investors.

From investor’s point of view, they have variety of securities to choose from tailored

according to their risk profile. Securitised products offer avenue for diversification of

portfolio. The risk of securitized product is insulated from the credit risk of the Originator.

Asset Reconstruction

Asset Reconstruction is another means of managing Non-performing assets. This

process helps extract maximum recovery value from asset at minimum cost. An Asset

Reconstruction Company has been given powers by SARFESI Act to

(i) Restructure the loan to suit cash flow of the borrowing entity

(ii) Sell or lease part/whole of the assets of the business to a third party

(iii) Change the management structure by appointing own directors(this was kept

in abeyance till recently, however in 2010, RBI has come out with guidelines

requiring Reconstruction companies to conduct proper due diligence through an

independent council before the final takeover)

(iv) Restructure the business operation – like expansion, diversification and closure

(v) Enforcement of security interest in accordance with provisions of the Act

(vi) Take possession of the secured asset in accordance with the provisions of the

Act

The Asset Reconstruction process is similar to Securitization. Firstly an SPV is formed

to acquire the Non–performing asset. The banks and financial institution selling the

Non– performing asset receives debentures or cash as consideration. The SPV issues

securities to investors and utilizes the finance raised to pay cash, or redeem debenture

issued, as the case may be to Banks and Financial institutions.

Determination of value of the distressed asset is an important process in the

Reconstruction process. Reconstruction companies have to arrive at fair value of the

asset acquired to derive maximum value from operations.

Similar to Securitization, reconstruction also relieves the bank of the burden of NPA and

allows them to allocate resources for core activities. It improves the liquidity position of

banks/FI

Requirements under SARFESI

The Securitization Act requires compulsory registration of Securitization and

Reconstruction companies under the SARFESI Act before commencing its business.

Further a minimum capital requirement is provided by requiring the company to possess

owned fund of Rs 2 crore or upto 15% of the total financial assets acquired or to be

acquired. The Reserve Bank of India has the power to specify the rate of owned fund

from time to time.

The act empowers the secured creditor to enforce security interest without the

intervention of court of tribunal not withstanding anything contained in section 69 or

section 69(A) of the Transfer of property act, 1882.

Under section 69 of the Transfer of Property Act, 1882 a mortgagee can take possession

of mortgaged property and sell the same without intervention of the court only in case

of English Mortgage. Thus we can see that the Securitization Act has removed the

restrictions previous imposed upon the creditor to approach court.

The Apex court in Mardia Chemical vs. Union of India examined various issues of the

Act which are discussed below

One contention of the petitioner was that section 13, dealing with enforcement of

security interest, empowered the secured creditor with unchecked arbitrary power since

there was no forum or mechanism to resolve any dispute which may arise in respect of

alleged default or overdue.

The Honourable Supreme Court pointed out that any law which did not give the other

party an opportunity to represent his case would be struck down by article 14 of the

Constitution. The court observed that a forum of internal mechanism must be evolved to

consider any objection raised by the borrower in reply to notice issued under section 13.

Another provision that can under scrutiny of the Apex court was section 17(2) which

required that 75% of the money due to be pre-deposited with Debts recovery tribunal to

prefer an appeal against the action taken by secured creditor or authorized officer under

the Act.

The supreme court held the condition of pre-deposit in the present case is bad

rendering the remedy illusory on the grounds that (i) it is imposed while approaching the

adjudicating authority of the first instance, not in appeal, (ii)there is no determination

of the amount due as yet (iii) the secured assets or its management with transferable

interest is already taken over and under control of the secured creditor (iv) no special

reason for double security in respect of an amount yet to be determined and settled (v)

75% of the amount claimed by no means would be a meager amount (vi) it will leave the

borrower in a position where it would not be possible for him to raise any funds to make

deposit of 75% of the undetermined demand. Such conditions are not alone onerous

and oppressive but also unreasonable and arbitrary. Therefore, in our view, sub-section

(2) of Section 17 of the Act is unreasonable, arbitrary and volatile Article 14 of the

Constitution.

Subsequently by an amendment in 2004 following changes were made in sub-section

(3), the following sub-section shall be inserted, namely:--

"(3A) If, on receipt of the notice under sub-section (2), the borrower makes any

representation or raises any objection, the secured creditor shall consider such

representation or objection and if the secured creditor comes to the conclusion that such

representation or objection is not acceptable or tenable, he shall communicate within

one week of receipt of such representation or objection the reasons for non-acceptance

of the representation or objection to the borrower:

Provided that the reasons so communicated or the likely action of the secured creditor

at the stage of communication of reasons shall not confer any right upon the borrower

to prefer an application to the Debts Recovery Tribunal under section 17 or the Court of

District Judge under section 17A";

The RBI had issued guidelines for securitization of standard assets by banks, financial

institutions and NBFCs in February 2006. The guidelines broadly dealt with ensuring

arms-length relationship between originator and the SPV, Capital treatment for credit

enhancement, amortization of profit/premium arising on account of sale, disclosure

by the originator and treatment of liquidity facility. RBI has treaded cautiously in the

aftermath of recent sub-prime crisis. SEBI has taken steps for public issue and trading of

securitized instruments in secondary market. In 2007, Securities Contracts (Regulation)

Amendment Act 2007 was amended to include “securitized instruments” in the definition

of securities, thus creating a legal framework for public issue and secondary market

trading of such instruments. Finally SEBI also released “Public Offer and Listing of

Securitized Debt Instruments Regulations 2008” in this regard.